Market & Economic Commentary

Economic and Investment Outlook Summary - 2026

Feb 10 2026

Each year, our investment team reviews forecasts from leading banks and investment houses, distilling their views into a clear, forward-looking perspective. At the start of 2025, we outlined several expectations for the year ahead. Some materialised as anticipated, including resilient economic growth and sustained AI-driven innovation, while others were tempered by renewed trade uncertainty and tariff-related pressures. With the benefit of hindsight, we can now assess how markets and the global economy responded before shifting focus to the opportunities and risks likely to define the investment landscape in 2026.

EXPECTATIONS AND OUTCOMES: 2025 IN REVIEW

Heading into 2025, forecasts centred on the anticipated effects of renewed US trade protectionism under the returning Trump administration. Tariffs on major trading partners were expected to fuel inflation, constrain monetary easing, and dampen global growth. In practice, while President Trump’s high-profile ‘Liberation Day’ tariffs triggered short-term volatility mid-year, their broader macroeconomic impact proved less damaging than initially feared. Central banks in developed economies shifted away from a higher-for-longer stance, delivering multiple rate cuts throughout the year. Japan stood alone in tightening policy further, though rates peaked below the widely expected 1% threshold.

Equity market outcomes diverged more sharply from expectations. Although the US entered the year as the preferred market, it did not lead global performance. Instead, emerging and Asian markets delivered the strongest returns, despite having been forecast to remain out of favour, supported by improving US–China trade sentiment and strong AI supply-chain demand. Korea and Taiwan were among the standout performers, due to their central role in AI hardware production. Optimism at the start of the year proved well-founded for Japanese equities, which went on to become the best-performing developed market in local currency terms. Returns were underpinned by supportive policy measures and continued improvements in corporate governance, although yen weakness tempered gains for UK-based investors.

European equities were expected to lag due to slower growth, ongoing manufacturing challenges, and elevated political risk, with the UK seen as the more resilient alternative given its services-heavy tilt. In practice, continental Europe held up better than anticipated, supported by fiscal spending and falling bond yields, even as political uncertainty persisted. Europe’s lighter technology exposure also proved less of a handicap than feared.

In the US, by contrast, it became a defining feature. Investors had expected leadership to broaden beyond large-cap technology into mid and small caps and a wider set of sectors, supported by deregulation and infrastructure spending. However, returns remained concentrated in technology and communication services, with limited contribution from elsewhere. As employment growth cooled, pricing power faded and tariff-related costs became harder to absorb, especially in consumer-facing sectors. The US still delivered positive absolute returns but finished 2025 at the back of the pack among major equity markets.

In 2025, fixed income markets largely reasserted bonds’ traditional role as a dependable source of income. This outcome was broadly consistent with expectations that policy rate cuts would lower shorter-dated yields. US Treasuries were the standout, proving the most attractive option among major sovereign markets and delivering the clearest upside surprise, supported by Federal Reserve rate cuts in the second half of the year.

UK gilts also performed well and broadly in line with expectations. Moderating wage growth and a cooling labour market underpinned returns, even as inflation remained above target. Across Europe, results were more mixed. Peripheral markets outperformed core bonds, narrowing the usual gap between the two and blurring the traditional core-periphery divide. Japan, by contrast, matched the downbeat outlook: government bonds generated negative returns as the Bank of Japan continued policy normalisation, while concerns about the longer-term fiscal trajectory weighed on sentiment.

Credit markets also delivered broadly as expected. Improving risk appetite supported spread tightening across both investment grade and high yield. Regional performance, however, did not align with the more upbeat outlook for European credit. In total return terms, US credit outperformed European peers, largely due to higher starting yields.

Gold was the standout performer among alternative assets, as widely expected, although few anticipated gains of the magnitude ultimately delivered. Demand was supported by investors seeking protection against inflation risks, alongside increased purchases from central banks diversifying away from currency reserves, uncertainty following the introduction of US tariffs, as well as heightened political risk and concerns about policy stability, including public pressure on the Federal Reserve chair in early 2026.

Commodity returns were mixed, with weaker energy prices offset by strength in precious and industrial metals. Hedge funds and infrastructure delivered solid returns and outperformed many traditional asset classes, broadly in line with expectations that alternatives would play a larger role in portfolio diversification. Despite bouts of tariff-related volatility, markets recovered from early losses and finished the year with positive returns. Market leadership also broadened beyond the US, reinforcing the case for diversification and balanced portfolio construction as investors look ahead to 2026.

2026: POSITIONING FOR THE FUTURE

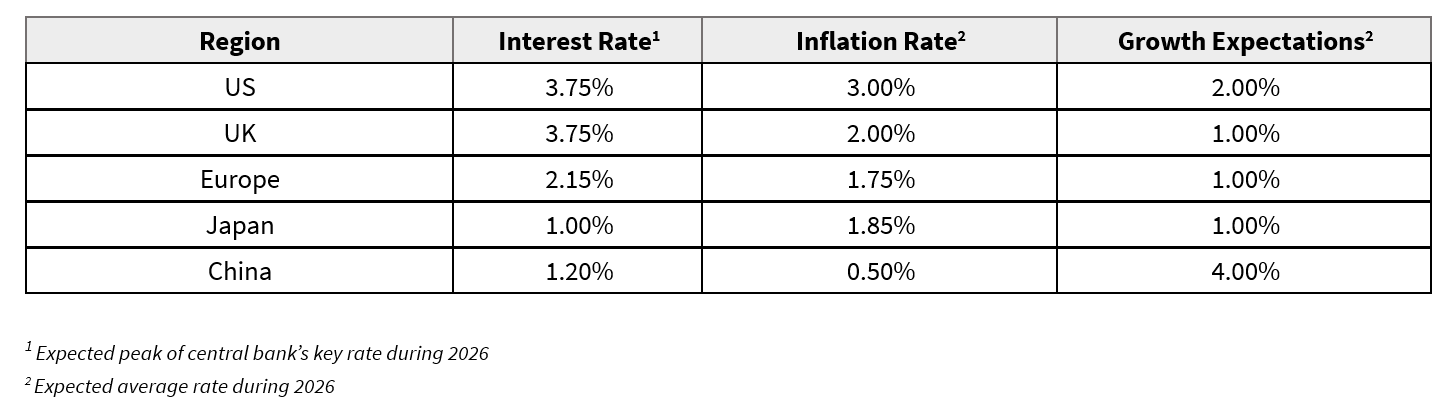

This year’s summary is presented in the table below.

MACRO AND POLICY

The prevailing outlook for 2026 is one of continuity rather than disruption. Global growth is expected to stay near trend, easing slightly from 2025 but supported by fiscal spending and ongoing AI investment. The US is seen expanding in the high-1% to mid-2% range, helped by policy tailwinds but tempered by tariffs and a cooling labour market. Europe should improve modestly on German-led fiscal support and easier financial conditions. The UK is likely to remain subdued amid fiscal tightening and weak productivity. Japan should grow steadily as policy normalises, while China slows toward the low-to-mid-4% range with targeted stimulus limiting the downside. Asia and emerging markets are expected to lead global growth.

Inflation is widely viewed as having peaked but proving slow to fade. This is most evident in the US, where trade barriers and tighter immigration policy keep wage and services inflation elevated around 3%. Europe is seen as closer to target, while softer demand in China remains disinflationary. The Federal Reserve is expected to cut further, though by less than markets currently price in. The European Central Bank is likely to stay broadly on hold or ease only marginally. The Bank of England has more scope to cut as growth softens. The People’s Bank of China should add support, and the Bank of Japan remains the key tightening outlier.

EQUITIES

Major institutions have come into 2026 supportive of equities. Their outlook is shaped by some regional divergence, limited valuation headroom in the US, and a market that remains heavily influenced by a small group of very large stocks. Concentration risk features prominently in major firms’ assessments. Citi argues that parts of the US market display bubble-like characteristics, a setup that could lead to more uneven leadership and higher volatility. Vanguard echoes the concern, noting that the expectations priced into large US technology names leave little room for disappointment. Even so, while the risks around the AI boom are well understood, many argue that the greater danger is being underexposed to such innovation. More broadly, there is wide agreement that productivity gains and the continued adoption of AI should remain supportive over the long term.

Away from the US, positioning is more selective. JP Morgan remains constructive on Europe but flags weak manufacturing momentum and persistent geopolitical risk as key constraints. Barclays is more favourable on the UK, arguing that its defensive sector mix offers useful diversification relative to continental Europe. In Asia, UBS points to China’s technology sector as a standout opportunity as fundamentals are expected to improve. Even where the long-term AI thesis is broadly embraced, the common message is to avoid an overly concentrated, single-theme approach and instead build exposure through diversification.

FIXED INCOME

The fixed income outlook for 2026 reflects a shift away from inflation control and toward policy normalisation. Morgan Stanley expects high-quality government bonds, particularly in the US, to rally into mid-year as central banks move toward easier policy, before yields edge higher later in the year. Deutsche Bank also anticipates developed-market yields trending higher through 2026 and views high-quality European duration as valuable. Goldman Sachs, however, expects yields to be broadly range-bound, with government bond returns driven largely by carry, but still sees shorter-maturity, high-quality duration as an effective hedge against key equity risks, including recession and a potential reversal of AI optimism. Taken together, these views imply front-end yields are capped by near-term rate cuts, while heavier government borrowing and issuance keep upward pressure on longer maturities, leaving the curve biased toward steepening.

In credit, the opportunity set looks increasingly issuer-specific, with Europe generally better supported than the US. JP Morgan argues that the market focus is shifting away from broad macroeconomic drivers and toward company-specific fundamentals. The firm expects credit spreads to widen in 2026, driven by heavier issuance linked to AI-related capital expenditures, as well as increased M&A and LBO activity. Morgan Stanley likewise anticipates wider US investment grade spreads, pointing to increased issuance from the tech sector. UBS sees less compelling risk-reward given rich valuations and expects modest spread widening that could constrain total returns even in its central case. While signs of stress remain limited and largely contained, credit is best positioned as an income allocation, implemented selectively with a bias toward higher quality and a consensus that spreads are more likely to widen than tighten from current levels.

ALTERNATIVES

In 2026, Gold remains a core safe-haven asset, underpinned by sustained central bank purchases and ongoing diversification demand. Many forecasts point to average prices in the $4,500 to $5,000 per ounce range or higher, although continued dollar strength could temper upside potential.

Deutsche Bank and Amundi emphasise gold’s role as both an inflation hedge and a strategic component of broader commodities exposure. Base metals, particularly copper, are expected to benefit from resilient economic growth and structurally rising demand linked to AI data centres, power grid modernisation, electrification and the energy transition.

Alternative assets, including private equity, hedge funds and infrastructure, are widely viewed as potential outperformers relative to many traditional asset classes. Deutsche Bank highlights that evolving regulatory frameworks are easing access to alternatives, expanding opportunities for portfolio diversification. Infrastructure remains a key priority, complemented by selective allocations to non-traditional exposures such as private equity.

OVERALL BASE CASE

Global growth should remain resilient in 2026, although it is likely to slow somewhat from recent levels. Central banks continue to ease policy, economic uncertainty gradually recedes, and the expansion extends without slipping into recession. We anticipate global GDP will grow modestly, with momentum building in the second half of the year. The US is expected to outperform. Growth should be driven in part by investment in artificial intelligence, fiscal measures including tax reductions and stimulus, and more accommodative financial conditions. Tariff effects may weigh on activity early in the year, but the overall impact appears contained. Europe is likely to stabilise, while Asia regains some forward momentum.

In this environment, risk assets stand to perform reasonably well. Global equities should deliver decent returns, credit markets remain supportive, and longer-term bond yields are likely to stay within a defined range. Artificial intelligence continues to act as a major secular force, driving capital expenditure and supporting growth in related companies without (yet) showing clear signs of a bubble. Downside risks are still present, including subdued business confidence, a softening labour market, geopolitical pressures, and the possibility that overly loose policy could lead to renewed inflation or asset price excesses. Overall, the base case remains positive. Further gains are possible, but it makes sense to maintain some protection through fixed income and alternative assets.

Written by Artem Dubas and Jonty Brooks

Cornwall

01326 210131

enquiries@taylormoney.com

London

By appointment only

020 7167 6690

enquiries@taylormoney.com

Let us call you back

Taylor Money Wealth Management provides a bespoke service for high-net-worth individuals looking for a long-term wealth management relationship. Let us get to know a bit more about your financial situation by getting in touch to request a call back.