Market & Economic Commentary

Economic and Investment Outlook Summary - 2025

Feb 11 2025

At the start of each year, our investment team reviews outlooks from major banks and investment houses, distilling insights into a clear and concise summary. Last year, we shared a similar summary of the key predictions, some of which played out as expected, while others fell short. With another year behind us, now is the perfect time to revisit these expectations and assess them against how the global economy and markets performed in response to real-world events. From there, we look ahead to 2025, and the expectations for the year ahead.

2024: A Year in Review

Heading into 2024, most forecasts predicted that interest rates in major economies had peaked and would start to decline. For the most part, this turned out to be true, as did expectations that Japan would lift rates above zero for the first time since 2007. Inflation was also expected to ease and settle just above 2% - which it did, remaining slightly above central banks’ targets. On the other side, economic growth was expected to slow across developed markets while picking up pace in China. This held true as well – except for the US. Despite a restrictive monetary policy, the US GDP grew quite substantially, defying the broader slowdown trend.

The US remained the preferred equity market geographically, and that confidence was well placed, with the S&P 500 emerging as the top performer. However, many institutions warned against an excessive overweight position to US equities, citing risks of overexposure to the ‘Magnificent Seven’ mega-cap tech stocks, which were already trading at high valuations. Financials and Consumer Discretionary – two of the eleven sectors in the S&P 500 – were expected to be the key contributors over the past 12 months. However, that prediction did not materialise. Consumer Discretionary ranked third, while Financials placed sixth. Instead, Information Technology and Communication Services emerged as the two leading sectors, driven by the meteoric rise of artificial intelligence (AI) and the demand for hardware supporting its development.

Europe (excluding the UK) was expected to see moderate gains and, while this was somewhat accurate, the region ultimately underperformed expectations. Economic momentum weakened over the year, with manufacturing struggling under high energy costs, weak export demand, and government-subsidised competition from China. The UK, though viewed more optimistically, fared only slightly better, finishing just above the broader European index. Initial post-election optimism provided a boost, but the autumn budget dampened sentiment, with larger-than-expected tax rises. Ongoing economic weakness kept both markets among the year’s underperformers. Japanese equities, on the other hand, were approached with caution – a view that was somewhat justified at the time given heightened volatility driven by expectations of central-bank rate hikes. However, despite these challenges, Japan still outperformed both Europe and the UK. Optimism about the end of deflation, a weak yen, and ongoing corporate reforms were the key drivers, providing strong tailwinds and making Japan the second-best performing market on our list.

Within fixed-income markets, yields were expected to decline across all maturities and particularly so in the US, Europe, and the UK, with short-term yields projected to fall more sharply than longer-term ones. In retrospect, this trend played out across all developed regions, but to different extents. By year-end, US Treasuries ranked among the weaker of the fixed income assets, though they still posted positive returns overall. Fiscal challenges, as expected, put pressure on long-duration bonds as they ended the year with losses. The Federal Reserve’s aggressive rate hikes further weighed on performance.

Closer to home, European bonds led the fixed-income market, ranking first in the list. This was driven by a weaker economic outlook, reinforcing expectations that the European Central Bank would take the lead in cutting rates - albeit gradually and with less-frequent adjustments. Compared with the US, the gap between short and long-term yields was far less pronounced. UK Gilts were the worst-performing sector, with longer-duration debt suffering the most as rising yields amplified its sensitivity to interest-rate movements. The autumn budget added further pressure, signalling increased future borrowing, while weak third-quarter growth fuelled concerns over greater government intervention - potentially leading to even higher debt issuance. High-quality fixed income such as government bonds and investment-grade credit were anticipated to offer the most attractive opportunities. Contrary to expectations, however, high-yield bonds dominated the market for yet another year. European higher risk bonds led the way, closely followed by US high yield.

Amid heightened geopolitical uncertainty, many firms maintained their commitment to alternative investments this past year, reaffirming the value we’ve long emphasised. Hedge funds performed best, as expected, while private equity achieved modest gains over the year. Commercial property lagged, with declines in the US and Asia-Pacific markets; Europe faring slightly better, yet still trailing private equity. Commodities were expected to deliver solid returns beyond their usual inflation-hedging role, and gold lived up to that promise by surpassing US equities for the year. So did silver and oil, which benefited from geopolitical tensions in Ukraine and the Middle East. Industrial metals struggled, however, with weaker global manufacturing dampening demand for copper, aluminium, and nickel. As we close the chapter on 2024, the early signs of 2025 are already setting the stage for an eventful year.

Outlook Summary for 2025

Please find this year’s summary in the table below. To see our more detailed outlook summary please click here.

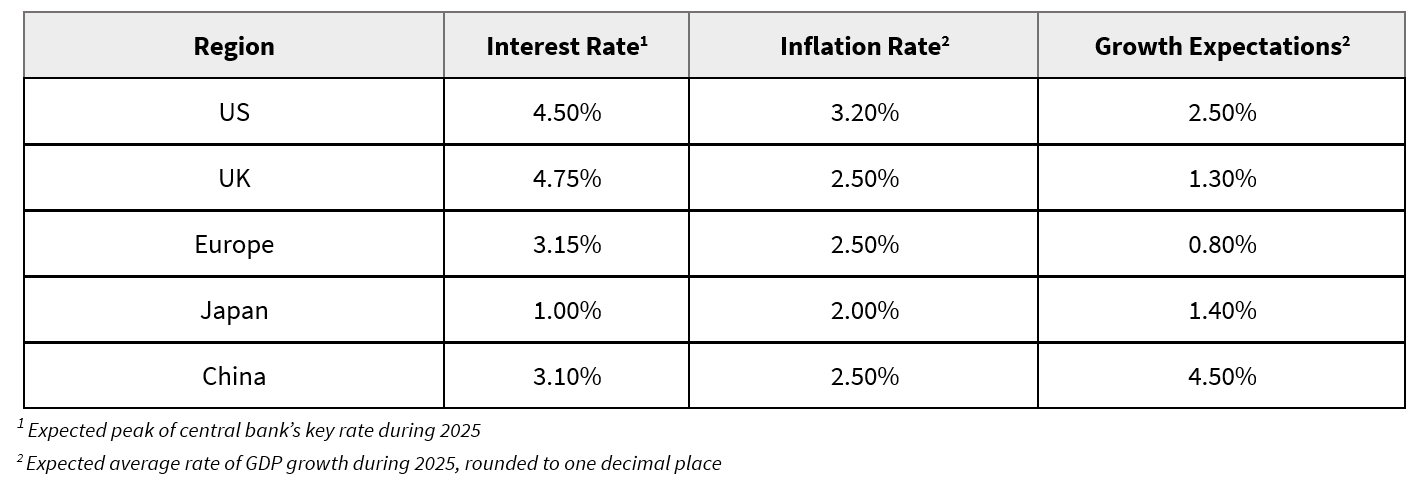

Economic Data - Aggregated Forecast for 2025

Economic Data

The return of Donald Trump to the White House dominates this year’s agenda, overshadowing the usual economic figures. While his pro-business philosophy strengthens the case for US assets, which is why most forecasts expect the US to lead G7 nations in growth, his hardline trade policies weaken the rest of the world. The recent executive order to impose tariffs on Canada, Mexico and China is viewed as bold and controversial, as additional inflationary pressures are precisely what central banks are trying to avoid. With inflation forecasts once again exceeding central bank target ranges for this year, interest rates are likely to stay higher for longer. However, there is a spread in expectations with some institutions expecting the federal funds rate to fall to 3.5% by the end of the year while others expect it to stay in line with the current level between 4.25% and 4.50%. Impacts of tariffs are expected to reverberate to the UK as well, although indirectly, primarily through the neighbouring economies of the European Union. Below-trend GDP growth for Europe and the UK is expected by the Bank of America, with the European Central Bank likely to hike rates more aggressively. Japan stands out as the only major economy expected to raise interest rates again, potentially reaching a 1% terminal rate by year-end as growth expectations are slightly better than in Europe. China’s outlook remains challenging, as anticipated fiscal and monetary stimulus may fall short of offsetting the impact of Trump’s protectionism.

Equities

US equities are once again the preferred choice for 2025, as most forecast the S&P 500 to end the year between $6,500 and $7,000, a percentage increase of between 8% and 16% respectively. UBS expects market leadership to expand beyond large-cap tech, with mid and small-cap dividend stocks taking a greater share of investor interest. Beyond the Technology sector, diversification into Financials, Industrials, and Energy is expected to gain momentum, driven by deregulation and increased infrastructure spending. European equities are expected to see slower growth as ongoing manufacturing challenges and political uncertainty remain the key risks. The UK market stands as a potential alternative, as its services-dominated economy offers some insulation from the difficulties affecting continental Europe. Japanese equities stand out among non-US developed markets. Attractive valuations, structural reforms, and rising corporate profitability point to more growth.

Fixed Income

In 2025, fixed income is reverting to its traditional role to provide income. Yield curves are expected to normalise, as shorter maturities are expected to decline with policy-rate cuts. US Treasuries remain the most attractive option, followed by German Bunds and UK Gilts. BNY forecasts 10-year Treasury yields to settle around 4% by year-end, while Deutsche Bank projects 10-year Bund yields to close at approximately 2%. The economic environment is presenting opportunities to lock in attractive yields. Caution is advised regarding concerns over fiscal deficits and longer-duration assets. Despite narrow spreads, European credit is expected to gain appeal, with investment-grade bonds remaining a strong choice as investor risk appetite improves. Japanese bonds remain out of favour due to the economic conditions mentioned previously.

Alternatives

Gold is widely seen as a strong safe-haven asset; however, its upside may be capped by a strong US dollar and its strong returns over the last few years. Oil will likely decline in value due to persistent oversupply and weak demand – Citibank predicts prices dropping as far as $60 per barrel. Base metals could benefit from a strengthening global economy and increased investment in tech infrastructure, including data centres and power plants. Private credit, hedge funds and infrastructure are expected to outperform traditional investments.

Overall Base Case

The consensus for 2025 is that the US is expected to remain the primary driver of global economic growth. Inflation is projected to remain around low single digits in most regions, though above central bank target levels of 2%, prompting fewer rate cuts. This is a relatively attractive environment for risk assets and, therefore, many continue to favour equities over bonds. However, there are risks to this view, particularly as Trump 2.0 is expected to implement major changes that will impact global trade in both developed and emerging economies. US large-cap technology stocks continue to be the most favoured, although many are pivoting into more balanced opportunities within small and mid-cap companies, as existing technology is expected to drive productivity gains, and therefore profits, across other sectors. Opportunities also exist within European and Chinese equities, however, concerns over weaker economic growth and trade tension make these regions potentially less attractive compared to the US. In other asset classes, private equity and infrastructure are gaining interest given their diversification properties, while gold is expected to continue its rise. Overall, the base case is supportive of remaining invested in risk assets however, as always, there are risks to the downside which should be closely watched.

Written by Artem Dubas and Jonty Brooks

Cornwall

01326 210131

enquiries@taylormoney.com

London

By appointment only

020 7167 6690

enquiries@taylormoney.com

Let us call you back

Taylor Money Wealth Management provides a bespoke service for high-net-worth individuals looking for a long-term wealth management relationship. Let us get to know a bit more about your financial situation by getting in touch to request a call back.