Insights & Knowledge

The resurgence of Whole of Life policies in estate planning

Aug 14 2025

In last year’s Autumn Budget, the UK government introduced a series of tax reforms aimed at increasing revenue without breaching key manifesto pledges on income tax, national insurance, or VAT.

Among the most consequential changes we have seen is those affecting Inheritance Tax (IHT). Specifically the tightening of agricultural and business reliefs from April 2026, as well as the inclusion of most pension death benefits in the value of a person’s estate from April 2027. Many of our clients have significant value in pensions, businesses and land, so these changes will directly impact them and their estate’s liability to IHT.

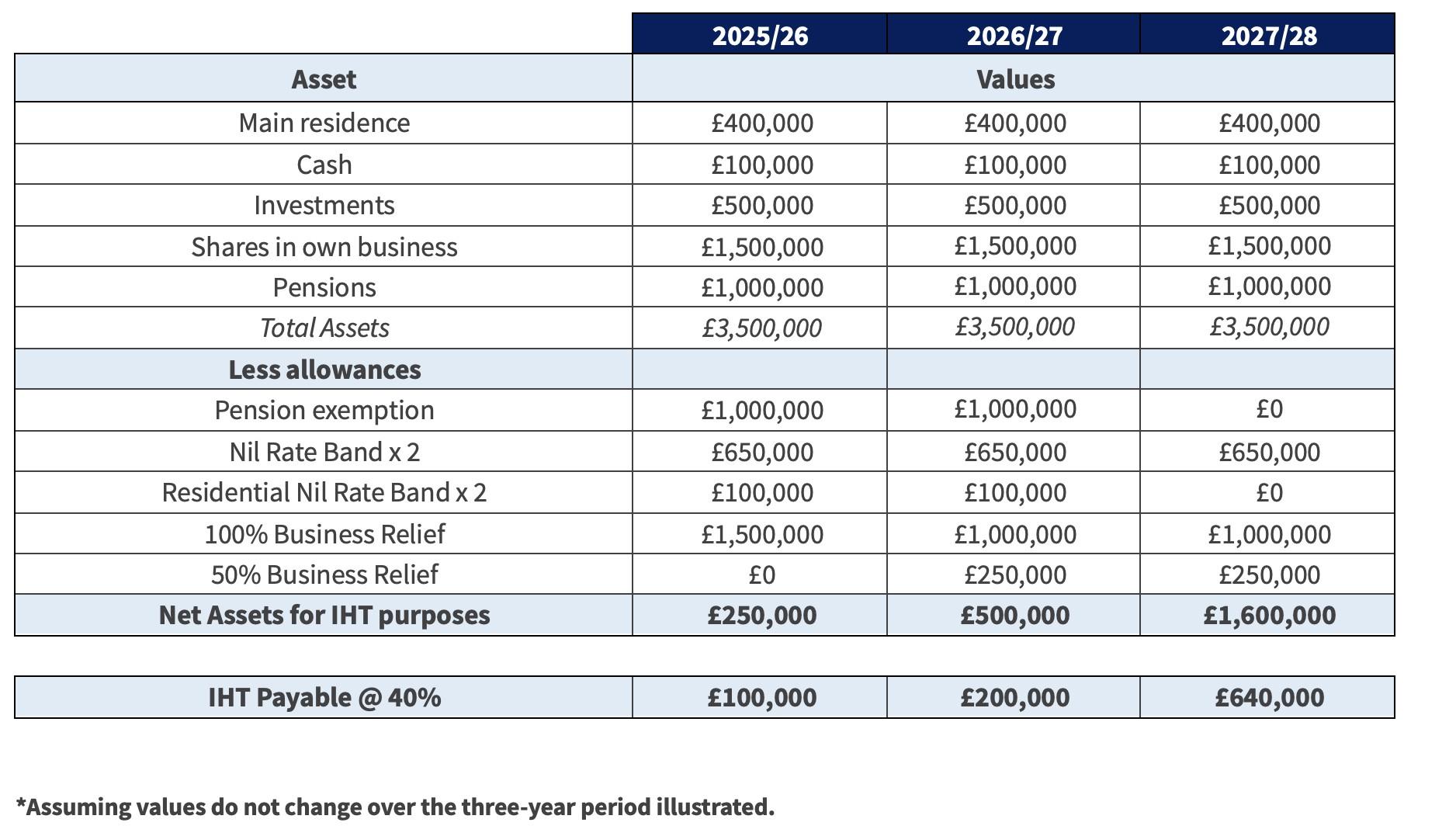

The below example shows how a couple with two full nil-rate bands and partial residential nil-rate bands might be impacted*.

We are finding that these developments are particularly relevant to our clients who were previously insulated from IHT exposure and who may now find themselves facing significant liabilities. As a result, we have seen a marked uptick in the consideration of Whole of Life (WOL) insurance policies as a planning tool.

What is a Whole of Life policy?

A Whole of Life policy is a permanent life insurance policy that guarantees a payout upon the policyholder’s death, regardless of when it occurs, provided premiums are maintained. Unlike term insurance, which only covers a specific period, WOL policies offer lifelong coverage, making them a dependable tool for long-term estate planning.

Why Whole of Life insurance matters for IHT planning

For many individuals with complex estates, liquidity at the point of death can prove to be a challenge. WOL policies address this directly:

- Guaranteed Liquidity: The policy provides a tax-free lump sum on death, ensuring that IHT liabilities can be met without the forced sale of illiquid or sentimental assets such as property, business interests, or private collections.

- Trust Structure: When written in trust(s), the policy proceeds fall outside the taxable estate. This not only avoids increasing the IHT burden but also ensures swift and direct access to funds for beneficiaries.

- By covering the IHT liability with the insurance proceeds, the estate can be passed on intact, preserving specific illiquid assets such as property or land for future generations.

Important considerations

Inheritance Tax planning is not static. Asset values typically appreciate over time and lifestyle demands, such as long-term care, philanthropy, or family support, can alter the shape of an estate. For this reason we highly recommend regular reviews to ensure the level of cover remains aligned with the estate’s projected IHT exposure.

With premiums payable for the remainder of someone’s lifetime, income-tax efficiency and cash flow management are key to ensuring the policies remain in place and are affordable.

Final thoughts

WOL insurance can be a strategic estate planning tool. In an evolving tax landscape, it offers certainty, control, and peace of mind for clients. When used correctly, especially in conjunction with trusts, WOL policies can significantly reduce the burden of Inheritance Tax and ensure a smoother transfer of wealth where you have planned for it to go.

If you have not reviewed your IHT strategy recently, or if you are unsure how recent legislative changes may affect your estate, please speak with your wealth manager to explore how we can support your long-term legacy goals.

Written by Paul Bannister

General Disclosures: This article is based on current public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. The information, opinions, estimates and forecasts contained herein are as of the date hereof and are subject to change without prior notification. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. The price and value of investments referred to in this research and the income from them may fluctuate. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur.

Cornwall

01326 210131

enquiries@taylormoney.com

London

By appointment only

020 7167 6690

enquiries@taylormoney.com

Let us call you back

Taylor Money Wealth Management provides a bespoke service for high-net-worth individuals looking for a long-term wealth management relationship. Let us get to know a bit more about your financial situation by getting in touch to request a call back.