Insights & Knowledge

Company Pension Contributions

Feb 17 2026

As featured in Business Cornwall, February 2026

Company Pension Contributions - The smart way for business owners to extract value

If you are a business owner in Cornwall, you may feel the last two Budgets have hit SMEs harder than ever. With new tax rules on the horizon, many owners are wondering, “How can I extract value from my business in the most tax-efficient way?”

We often encounter successful business owners with growing cash balances in their company. A healthy amount of cash in any business is sensible as it can help fund emergency expenditure, growth and expansion. Beyond this however, accumulating cash can become inefficient and a great deal of thought is often given as to how best to draw some of this hard-earned profit from the company.

The recent changes by the Government have made passing on assets and extracting profit or value from a business more expensive:

- Employer National Insurance (NI) increased from 13.8% to 15% in 2025/26

- Dividend tax increasing by 2% across all tax bands from 2026/27

- Business Property Relief: A new limit to the value of businesses qualifying for 100% BPR from 2026/27

- Business Asset Disposal Relief (BADR): The BADR tax rate increased from 10% to 14% from 6 April 2025, and is increasing to 18% from 6 April 2026.

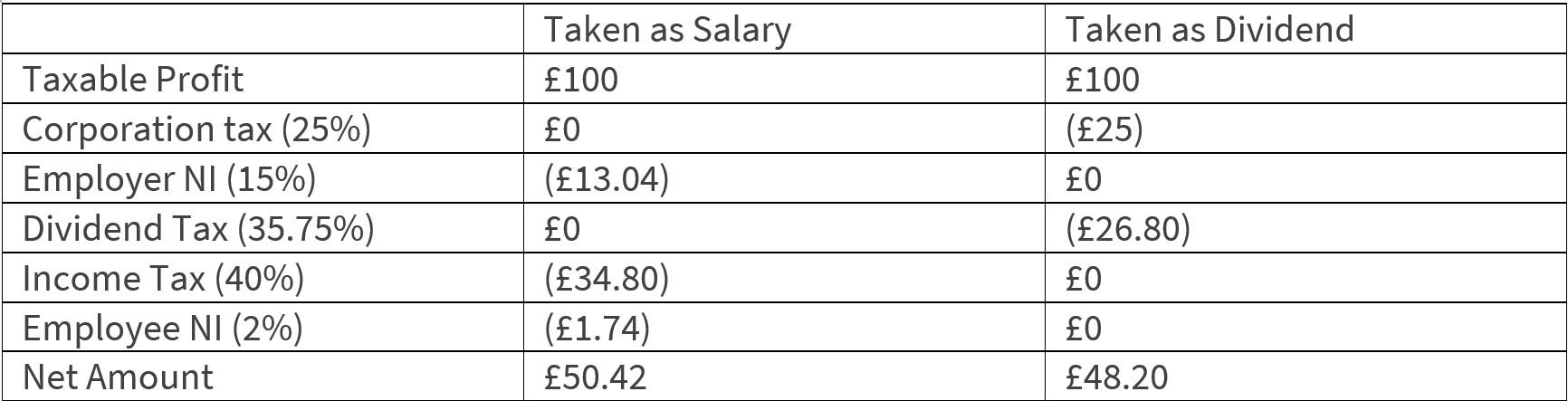

Salary vs Dividend: What is left after tax?

Let us now look at what is left after an owner draws £100 of profit, assuming a corporation tax rate of 25% and higher rate income/dividend tax:

In both scenarios, you will receive around 50% of your profit net of tax.

Company pension contributions

These tax increases have made company pension contributions more attractive than ever. When your business pays directly into your pension, the contribution is paid gross(before tax)and can be treated as a business expense (subject to your accountant’s approval). This means you can extract the full £1 of profit for your long-term benefit. This equates to a day one return of around 100% or 7% annualised for 10 years. In addition, once in your pension, the monies grow free of capital gains and income tax.

Making the most of your allowances

- Each business owner can contribute up to £60,000 per annum to their pension, and may also be able to use unused allowances from up to three previous tax years.

- A pension contribution of £60,000 could result in a tax saving of more than £30,000.

- Even with upcoming changes to pension tax rules on death, pensions continue to offer the most tax-efficient way to draw capital from your business.

If you would like to understand your options in more detail, contact Taylor Money Wealth Management:

01326 210131

Philip Feast is a Director and Chartered Financial Planner at Taylor Money Wealth Management. Article correct as of 6 January 2026.

General Disclosures: This article is based on current public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. The information, opinions, estimates and forecasts contained herein are as of the date hereof and are subject to change without prior notification. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. The price and value of investments referred to in this research and the income from them may fluctuate. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur.

Cornwall

01326 210131

enquiries@taylormoney.com

London

By appointment only

020 7167 6690

enquiries@taylormoney.com

Let us call you back

Taylor Money Wealth Management provides a bespoke service for high-net-worth individuals looking for a long-term wealth management relationship. Let us get to know a bit more about your financial situation by getting in touch to request a call back.